Revenue increased to $72.8 million with 8% Growth in the IT Segment

PLAINVIEW, N.Y. March 30, 2018 – Vaso Corporation (“Vaso”) (OTCMKTS: VASO) today reported its operating results for the three months and year ended December 31, 2017.

“We are pleased to announce a record revenue of $72.8 million for the fiscal year 2017. This growth was small but very significant since it was achieved in spite of a major decrease in commission revenue from the professional sales service segment,” stated Dr. Jun Ma, President and Chief Executive Officer of Vaso Corporation. “Revenue in our IT segment grew 8% from the previous year to $42.6 million, accounting for 59% of the Company’s total revenue in 2017, a testament of our growth strategy at work.”

“It is important to understand that, while revenue in the professional sales service segment took a hit in 2017 due to lower delivery volume of underlying diagnostic imaging equipment in the year, our performance in this segment remained outstanding, with a 7% year-over-year growth in equipment order volume,” Dr. Ma continued. “The combined effect of higher order booking and lower equipment delivery in the year led to a substantial escalation of deferred revenue in the segment, to $22.1 million at the end of 2017 from $18.5 million a year ago. This provides a strong assurance of future business, because the deferred revenue, recorded upon order booking, corresponds to roughly half of the commissions to be earned, the full amount of which will be recognized when underlying equipment and services are delivered to the customers.”

“In addition to a strong deferred revenue recorded on the balance sheet, we also saw a large increase – by $16.5 million, or 39%, year-over-year – to $59.3 million in the backlog of the IT segment. Therefore, while we experienced a net loss in 2017 compared to a net income in 2016, we expect to see continued sales growth in 2018 with improved profitability. Last but not least, our operations continue to generate healthy positive operating cash flow of $1.6 million in 2017, further strengthening the Company’s financial position with cash balances of approximately $9 million as of March 23, 2018,” concluded Dr. Ma.

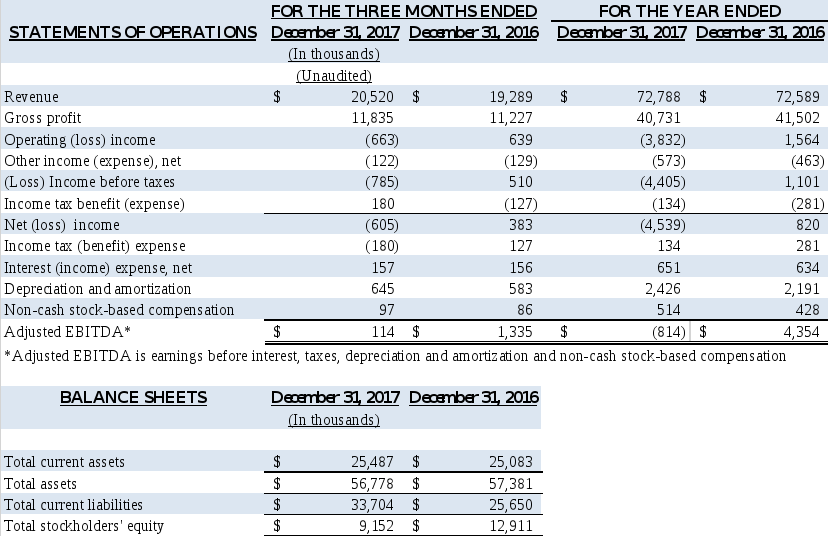

Financial Results for Three Months Ended December 31, 2017

For the three months ended December 31, 2017, revenue increased 6.4% to $20.5 million from $19.3 million for the same period of 2016, due primarily to the increase of $1.2 million or 12.3% in revenue in our IT segment, while revenue in our professional sales service and equipment segments was relatively flat in the fourth quarter 2017, compared to the fourth quarter 2016.

Gross profit for the fourth quarter of 2017 increased 5.4% to $11.8 million, compared with a gross profit of $11.2 million for the fourth quarter of 2016. This increase is primarily the result of the increase in revenue in the IT segment resulting in an increase in segment gross profit of $0.5 million, and small increases in gross profit in the professional sales service and equipment segments.

Selling, general and administrative (SG&A) expenses for the fourth quarter of 2017 increased 17.7% to $12.3 million, compared to $10.4 million for the fourth quarter of 2016. The increase is primarily attributable to an increase in personnel costs in the professional sales service and IT segments. SG&A expenses were 59.8% of revenue in the fourth quarter of 2017 compared to 54.1% of revenue for the same quarter of 2016.

Net loss for the three months ended December 31, 2017 was $0.6 million, compared with a net income of $0.4 million for the three months ended December 31, 2016.

Financial Results for Year Ended December 31, 2017

For the year ended December 31, 2017, revenue increased $0.2 million to $72.8 million, compared with $72.6 million for the year 2016. Revenue in our IT segment increased 7.9% to $42.6 million for the year ended December 31, 2017, compared to revenue of $39.4 million in 2016, due to increases of $1.4 million and $1.8 million in revenue at NetWolves and VHC-IT, respectively. Commission revenues in our professional sales service segment decreased by 7.3% to $26.4 million as a result of lower equipment deliveries compared to 2016. Equipment segment revenue for the year 2017 decreased by 18.5% to $3.8 million, compared to $4.6 million in 2016, principally due to the decrease in volume of EECP® equipment sales and a decrease in sales at our Biox subsidiary.

Gross profit for the year ended December 31, 2017 decreased 1.9% to $40.7 million, from $41.5 million in 2016. The decrease was due primarily to a decrease of $1.7 million in our professional sales service segment and a decrease of $0.4 million in our equipment segment as a result of the lower revenues in these segments, offset by an increase of $1.3 million in our IT segment resulting from the increase in revenues and improved profit margins in this segment.

SG&A expenses for the year ended December 31, 2017 increased 10.7% to $43.6 million, or 59.9% of revenue, compared with $39.4 million, or 54.3% of revenue, for the same period in 2016. The increase resulted primarily from an increase in personnel costs in the professional sales service segment and an increase in personnel costs and bad debt expense in our IT segment, partially offset by a decrease in SG&A costs in the equipment segment.

For the year ended December 31, 2017, the Company had a net loss of $4.5 million, or $0.03 per common share, compared with a net income of $0.8 million, or $0.01 per common share, for the year ended December 31, 2016.

Adjusted EBITDA (earnings before interest, taxes, depreciation and amortization, and share-based compensation) was negative at $0.8 million for the year ended December 31, 2017 compared to positive Adjusted EBITDA of $4.4 million for the year ended December 31, 2016. The decrease was primarily the result of the net loss in 2017, partially offset by higher depreciation in 2017 compared to 2016.

Net cash provided by operating activities was $1.6 million and $5.2 million for the year ended December 31, 2017 and 2016, respectively. Net cash decreased to $5.2 million at December 31, 2017, compared to $7.1 million at December 31, 2016. The decrease in cash is the net effect of positive cash provided from operations reduced by expenditures for equipment and software as well as repayment of debt. As of March 23, 2018, the Company’s net cash was approximately $9 million.

Deferred revenue increased substantially, at approximately $23.1 million as of December 31, 2017, an increase of $3.7 million compared to deferred revenue at December 31, 2016. The deferred revenue will be recognized in the future when the underlying equipment or services are delivered and accepted at the customer site. Our shareholders’ equity decreased to $9.2 million as of December 31, 2017 from $12.9 million as of December 31, 2016.

About Vaso

Vaso Corporation is a diversified medical technology company with several distinctive but related specialties: managed IT systems and services, including healthcare software solutions and network connectivity services; professional sales services for diagnostic imaging products; and design, manufacture and sale of proprietary medical devices.

The Company operates through three wholly owned subsidiaries:

Additional information is available on the Company’s website at www.vasocorporation.com.

Summarized Financial Information

Except for historical information contained in this report, the matters discussed are forward-looking statements that involve risks and uncertainties. When used in this report, words such as “anticipates”, “believes”, “could”, “estimates”, “expects”, “may”, “plans”, “potential” and “intends” and similar expressions, as they relate to the Company or its management, identify forward-looking statements. Such forward-looking statements are based on the beliefs of the Company’s management, as well as assumptions made by and information currently available to the Company’s management. Among the factors that could cause actual results to differ materially are the following: the effect of business and economic conditions; the effect of the dramatic changes taking place in IT and healthcare; continuation of the GEHC agreements; the impact of competitive technology and products and their pricing; medical insurance reimbursement policies; unexpected manufacturing or supplier problems; unforeseen difficulties and delays in the conduct of clinical trials and other product development programs; the actions of regulatory authorities and third-party payers in the United States and overseas; and the risk factors reported from time to time in the Company’s SEC reports. The Company undertakes no obligation to update forward-looking statements as a result of future events or developments.

© 2026 Vaso Corporation | Terms of Service | Privacy Policy